")

A practical guide for community business owners

Most business owners know they should have an estate plan. Most do not have one that actually works.

The Numbers That Should Get Your Attention

That is an average IHT saving of fourteen percent per estate. On the larger estates, over £20M, we have found over £4.5M of savings per estate. None of that is theoretical. It is the result of starting the conversation early enough to do something about it.

If you plan in advance, there is potential for hundreds of thousands of pounds in savings. The problem is most people lack urgency until it is too late.

1. What is Estate Planning?

Put simply, estate planning is making sure what you have built gets to the right people, in the right way, with as little tax, delay and disruption as possible.

For business owners it is not straightforward. You are likely to have company shares, property, loans, pensions, family arrangements and they all interact with each other in ways that a standard approach will not pick up. We have seen poorly planned estates leave families with unexpected tax bills, force the sale of a business that nobody wanted to sell, and trigger family disputes that could easily have been avoided.

Inheritance tax gets most of the attention but it is only part of it. Estate planning is about protecting your family, protecting the business, and having a clear plan in place for when you are no longer around or no longer able to make decisions yourself.

2. Is Your Estate Exposed? The Red Flags

As a couple, a review is overdue if any of the following apply. If you are single, most of these thresholds halve:

- Non-business estate approaching £1M

- Total estate over £2M

- Business shareholding worth over £5M

It is also worth noting that if assets within a couple are not owned equally, there may be exposure even where the total estate appears within threshold. And as the business grows, so does the exposure, a good year can push you over one of these limits without you realising.

IHT laws are changing. The current government has particularly targeted inheritance tax, and the rules around business property relief have been updated. We recommend reviewing your position annually, even if it is just a quick check.

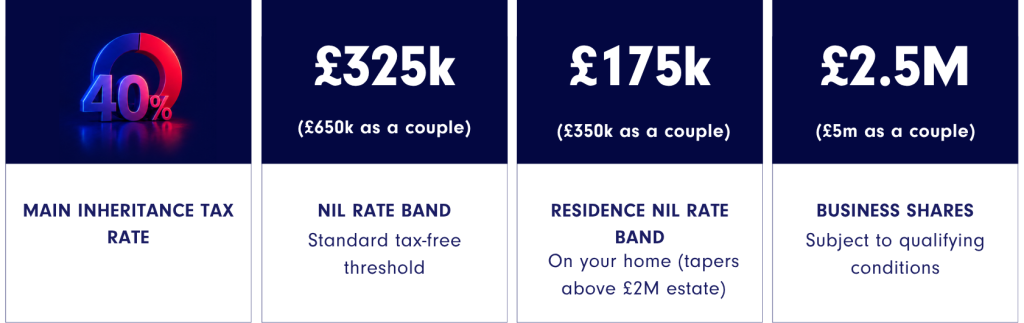

3. The Basics: Allowances and Rates

The headline IHT rate is 40% on everything above your allowances. Here is what those allowances look like:

4. How to Mitigate IHT

Gifting

Gifting is one of the most straightforward ways to reduce your estate. If you make a gift, it falls outside your estate after seven years, though tapering relief starts to reduce the tax charge from year three.

This is not something to leave too late. Seven years is a long time, and the options available on your deathbed are expensive, limited and unlikely to achieve the savings you might hope for. A proper gifting strategy agreed in advance can make a significant difference. HMRC applies strict anti-avoidance rules, so any arrangement must be genuine and commercially motivated.

One lesser-known relief worth flagging is the Exemption for Gifts from Surplus Income (Form IHT403). If you regularly give away money from your surplus income, those gifts can fall outside your estate immediately. Documentation is critical: keeping records as you go makes it far easier for your executors when it matters.

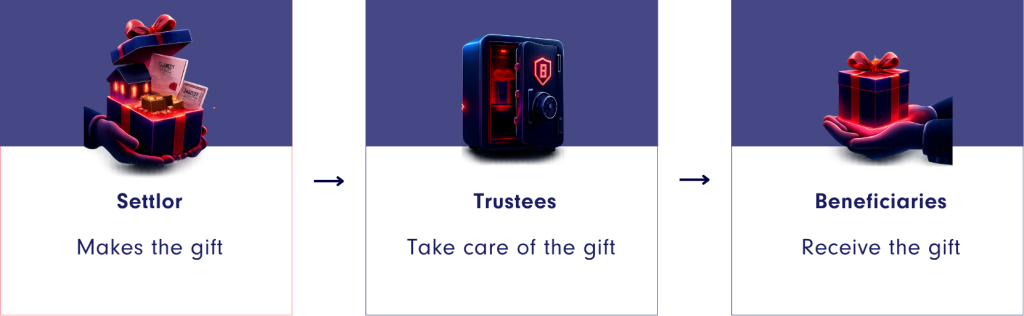

Trusts

Assets placed into a trust sit outside your estate for IHT purposes though the seven-year rule still applies to the initial gift. A trust is made up of three parties: the settlor (who makes the gift), the trustees (who manage it), and the beneficiaries (who receive it).

Trusts are not just an IHT saving mechanism. Used correctly, they can achieve income tax efficiencies by passing dividends to lower-rate beneficiaries, provide asset protection, and allow assets to be released in a controlled way over time. We've found that many community families have trusts in place that are not being used to their full potential, often because people are not clear on how they are supposed to work.

If you have a trust that is sitting dormant or that you do not fully understand, it is worth having a conversation. There may be significant value in what you already have in place.

Family Investment Companies

Family Investment Companies (FICs) have become increasingly prominent in estate planning. They can be particularly useful where a business has been sold and the proceeds held as tax-paid cash. By setting up a FIC in the right way, the value can accrue to the next generation while the original owner retains control and income. The compliance requirements are manageable if kept on top of from the outset.

Care Home Fees

One of the most common questions the team receives is whether anything can be done to protect assets from care home fees. The answer is yes, but it requires planning well in advance. Deliberate deprivation of assets is tightly regulated, and any arrangement that looks artificial will be challenged. The approach that works is making genuine gifts and trust arrangements ahead of time, for legitimate commercial reasons, with proper documentation in place.

5. How Your Estate is Distributed

This is one of the most personal aspects of estate planning and one of the most important to get right. The key principle is this:

| Fair is not always equal. But it has to be explainable. And defensible. |

Equal distribution between children feels simple and avoids difficult conversations. But it often does not reflect the reality of the family situation and when it does not, it can cause serious relationship damage and, in some cases, force outcomes nobody intended.

A real example: a well-meaning father left his estate equally between his son and three daughters. Ninety-five percent of the estate was in the business. The daughters, who had nothing to do with the business, needed cash. The son was left with no choice but to sell the business to pay them out, entirely the opposite of what was intended.

Examples Where Equal May Not Be Right

Business succession

Where sons are involved in the business and daughters are not, it usually makes sense to structure things so the business passes to those running it, with the estate squared up through other assets.

Prior lifetime gifts

If shares or cash have already been gifted to some family members during your lifetime, those gifts should be taken into account when the Will is structured.

Different financial need

£200k means a lot more to a child with a large mortgage than to one with a £20M estate and no debt. Clear communication is essential, this may not be well received, but it reflects genuine fairness.

Not in fellowship

Where family members are not in fellowship with the brethren, it is important that they are treated fairly in the Will. However, careful thought needs to go into which assets they receive. Business shares, for example, should generally not pass to someone who has no involvement in or connection to the business.

Carer child

Where one child has acted as a carer in the later years of your life, additional recognition in the Will is often appropriate and expected.

Blended family

Where there has been more than one marriage, the surviving spouse should retain the use of assets in their lifetime but assets should pass to the bloodline of the originally deceased on second death.

Risky circumstances

Where a child is not financially responsible or faces unstable circumstances, a trust may be a better vehicle than a direct inheritance, allowing assets to be released in a controlled way.

A Letter of Wishes can be placed alongside your Will to explain the reasoning behind your decisions. This does not change what the Will says, but it gives family members an understanding of why decisions were made, which significantly reduces the risk of disputes.

6. Wills: What Every Business Owner Needs to Know

What happens without a Will

Without a Will, the law decides for you. If you are married with no children, your spouse gets everything, fine. But if you have children, it splits: your spouse gets the first £322k, all personal possessions, and half the remaining estate. The children share the other half equally. That might sound reasonable until you factor in business shares. They could end up with family members who have nothing to do with the business and probably should not be shareholders.

Community-specific requirements

Your solicitor must understand the requirements of the community. Community executors must be appointed, and the Will must be signed off in the name of the Lord Jesus. Not all solicitors are familiar with these requirements, UBTA can recommend solicitors with the relevant experience.

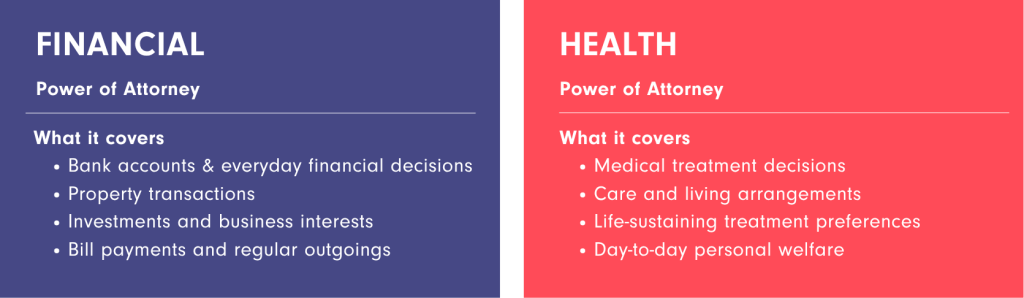

7. Power of Attorney

A Lasting Power of Attorney (LPA) appoints someone to make decisions on your behalf if you lose the capacity to make them yourself. There are two types:

Both only come into force if you lose capacity. Until that point, you remain in full control. But they must be set up before they are needed, you cannot grant an LPA after losing capacity. For business owners, this is particularly important. If you are a controlling shareholder and become incapacitated without an LPA in place, decision-making in the business can grind to a halt. This applies at any age as anything can happen to anyone.

When choosing an attorney, pick someone you trust who understands how you think. It is worth reviewing the appointment periodically, an attorney who is significantly older than you may themselves lose capacity before you do.

8. The UBTA Approach

UBTA follows a simple three-stage process for estate planning, led by Lewis Chaplin as Private Client Manager. The focus is on straightforward, understandable solutions with a long-term outlook and education throughout, so that whatever is put in place is fully understood by you and your family.

10. Where to Start

If your estate has not been reviewed for a while or if this guide has confirmed that a review is overdue, the right next step is a conversation.

We are offering a free initial consultation that covers a full evaluation of your estate, confirmation of your current IHT exposure, and the start of a discussion about how to protect what you have built.

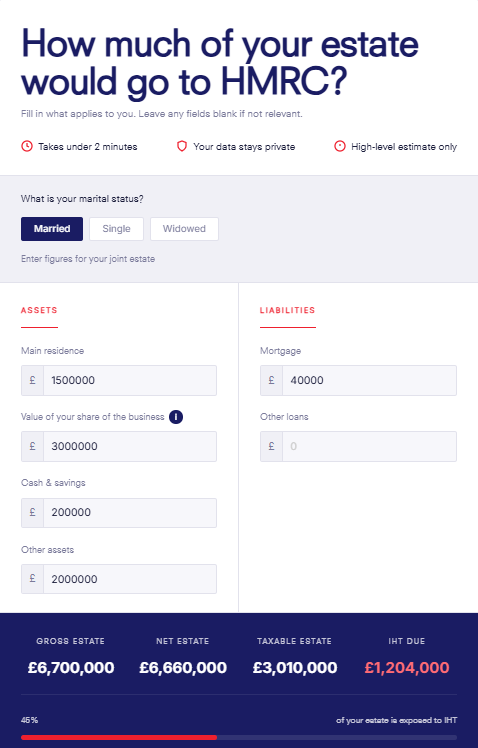

Free IHT Estate Calculator

As shared in the webinar, here's the IHT Calculator to help you get a high-level estimate of your IHT exposure. Enter your estate details and it will calculate your position in seconds. If you have already submitted a consultation request through the calculator, we will be in touch shortly.