")

This whitepaper is based on the content delivered in our live webinar, drawing on many years of work with project businesses across construction, engineering, fit-out and professional services.

Project businesses face a reporting challenge that most other business models do not. Revenue is lumpy, costs arrive out of sequence, and the gap between what is happening on site and what appears in the accounts can be wide enough to fundamentally mislead the people running the business.

At UBTA, we work with project businesses across a range of sectors and sizes. One thing is consistent: lack of communication and visibility on individual project numbers is invariably leaving margin on the table. The P&L and balance sheet alone cannot tell you whether you are winning or losing on any given project.

This whitepaper sets out the key principles, frameworks and practical approaches that form the backbone of good project reporting, the same methodology we deliver for our clients.

Understanding Your Project Business Model

No two project businesses are the same, and this matters enormously when it comes to accounting and reporting methodology. We rarely come across two businesses to which we can apply an identical approach.

We typically observe three broad categories:

- Short delivery timeframe - projects completed in under two months. Revenue and cost recognition is relatively straightforward and can often be done at project completion without distorting the P&L significantly.

- Longer delivery timeframe - projects spanning more than two months. These require a clear methodology for recognising revenue and costs progressively as work is delivered.

- Project-based sales with standard delivery - businesses that sell on a project basis but deliver standard stock items or products. These may not require full project accounting treatment but will still benefit from project-level visibility.

Some project businesses are also manufacturers, which adds another layer of complexity. The approach to accounting and reporting will vary significantly depending on your specific model, which is why a bespoke methodology is always required.

The Commercial–Financial Connection

Before covering the technical accounting elements, it is worth making a point that is fundamental to everything else: the financial and commercial functions of a project business need to operate as one.

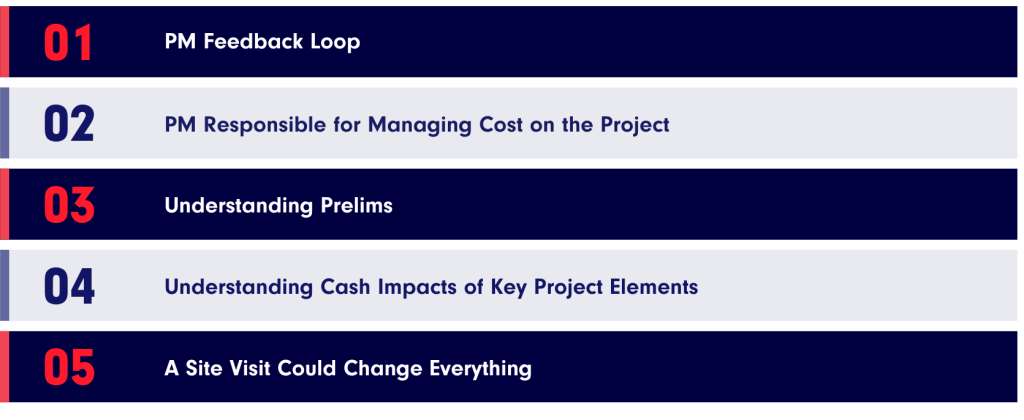

The project manager’s role in financial performance

One of the most critical roles in a project business is that of the project manager or contracts manager. We have often found that these individuals are responsible for delivering a project to programme, but are not held accountable for managing the cost budget. This creates a gap between the person with the greatest influence over outcomes and the financial performance of the project.

It is absolutely critical that one person takes ultimate responsibility for delivering the project to cost budget, from the point at which the estimate is handed over to delivery. The project manager is generally the best person to own this accountability.

Prelims and the danger of blanket assumptions

Preliminary costs - site setup, supervision, welfare facilities are often estimated using a generic percentage across all project sizes. We worked with one business using a blanket 8% for prelims across projects ranging from £200k to £2m. The reality is that prelim costs as a proportion of a smaller project are considerably higher than on a large one. Using a blanket rate means under pricing smaller projects and overpricing larger ones, both of which have a direct impact on GP.

Cash timing and the site visit

Understanding the cash profile of a project starts before delivery. Submitting a valuation in week two of a month rather than week three can make the difference between a project running cash flow positive or negative in that period.

Equally, investing in a thorough site visit before a project begins can avoid costly surprises. We had a specific example with one client who fabricated a bespoke tea point off-site, shipped it to London, and only discovered on arrival that it would not fit in the lift. It had to be cut in half, carried up in pieces, and reassembled on-site by a specialist joiner, a significant cost overrun that a pre-project site visit would have prevented entirely.

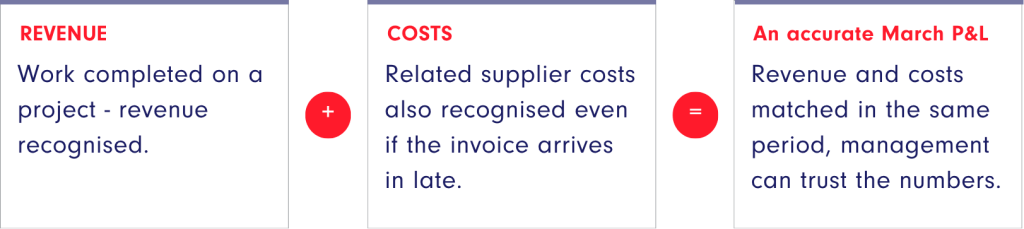

The Matching Principle

At the heart of accurate project reporting is a fundamental accounting concept: the matching principle.

An accounting concept that dictates that expenses must be recorded in the same period as the revenues they helped generate. It ensures financial statements reflect a business's true profitability over a specific timeframe.

The Four Key Balance Sheet Lines

For a project business, the health of your project accounting is visible in four specific lines on the balance sheet. Understanding what each one means and what direction it should be moving in is essential for any project director or finance lead.

Calculating WIP

Many project businesses are over-focused on calculating WIP as a mechanical exercise. We encourage a different way of thinking about it: instead of starting with WIP, start with revenue recognition.

Revenue recognition means determining the value of the work that has genuinely been delivered to the client and recognising that value in the P&L. WIP is simply what is left over once that decision has been made

The three-step approach

Short vs. long delivery timeframes

For businesses with a high volume of low-value, short delivery projects, it may be appropriate to recognise all revenue and costs at project completion. This simplifies administration, though it can make monthly results appear lumpy. Forecasting becomes critical in this scenario to provide context.

For businesses with longer delivery timeframes, a progressive methodology is needed. A common approach is to apply percentage completion to defined project phases, recognising revenue and cost in proportion to the work completed at each stage.

Payment applications and retentions

Businesses operating on a payment application model need to consider whether applications are typically accepted without challenge. Where there is a consistent track record of full acceptance, it may be appropriate to recognise revenue on application. Where there is routine dispute or reduction, a more conservative approach is warranted.

Retentions should be treated with a clear policy. The key decision is whether to recognise retention revenue upfront alongside the related costs, or to defer it until the retention is released. Whichever approach is adopted, it must be applied consistently and documented in a formal revenue recognition policy.

Project Level Financial Reporting

The P&L and balance sheet are essential, but for a project business they are not enough on their own. They show the aggregate result. They cannot tell you which projects are winning, which are struggling, or why margins moved month on month. We often say that project-by-project performance reporting is more important than the management accounts themselves. A project business is, in essence, a collection of individual P&Ls the management accounts are simply the sum of all of them.

Forecasting Project by Project

Project businesses are, by their nature, lumpy — in revenue, in GP, and in cash. Trying to forecast without drilling into the detail of individual projects produces numbers that are not useful for decision-making.

Each project should have its own forecast, including a cost to complete. This gives context to the current period results and provides forward visibility on both profit and cash.

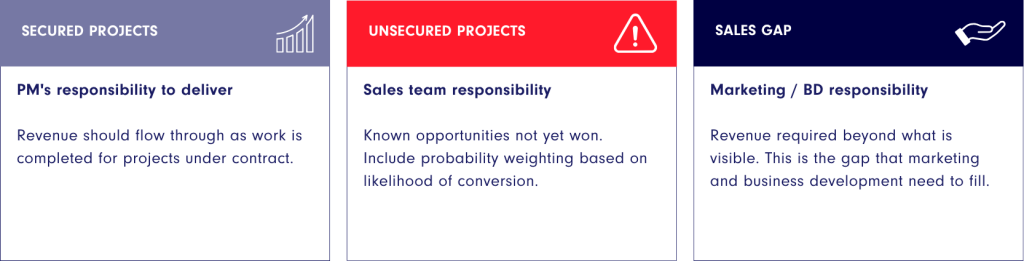

Building the revenue forecast

We recommend building the revenue forecast with three distinct components:

This breakdown makes accountability clear across the business and highlights where attention is needed to close the gap.

Cash flow visibility by project

It is also critical to maintain a cash flow forecast on a project-by-project basis. This serves two purposes: at the sales stage, it allows the business to evaluate whether taking on a project will have a detrimental impact on overall cash flow; during delivery, it gives project managers the visibility to take action.

When a project manager knows that a valuation date is approaching, they can prioritise completing the work needed to be included in that application. That decision alone can move a cash receipt forward by 30 days, a meaningful difference at a business level.

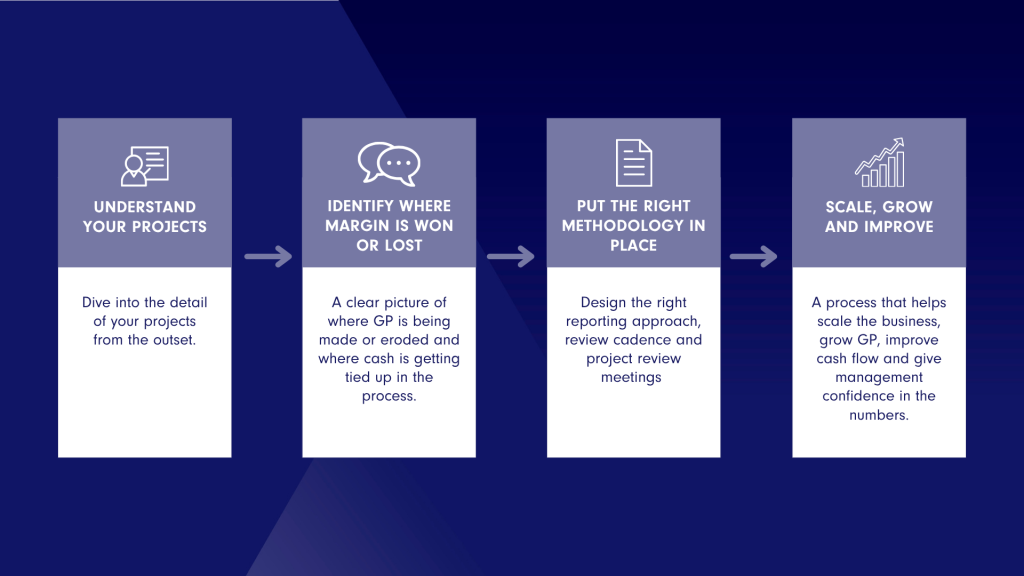

The UBTA Approach

When we work with a project business, our starting point is always to understand what is actually happening — not to impose a pre-built solution. Every business has its own processes, systems and commercial realities, and the methodology needs to fit around those.

If you would like to discuss your project reporting and whether it is fit for purpose, we would be very happy to have that conversation.

Click here to book a consultation and register your interest for a project seminar.

The content of this whitepaper is general in nature and does not constitute specific financial or accounting advice. Your situation may require tailored input. Please contact us to discuss your specific circumstances.